Rule 4 Deduction: Explained

- What's a Rule 4 deduction and when does it apply?

- How will I know if a Rule 4 has been applied to my bet?

- How is the Rule 4 amount calculated?

- Do you have an example calculation?

- What happens if there’s more than one non-runner?

- What about ante-post bets?

- Why is it called a ‘Rule 4’?

- Terms and Conditions

What's a Rule 4 deduction and when does it apply?

If there are one or more non-runners (withdrawn horses), your winnings may be less than you expected.

When a horse withdraws from a race, the remaining horses now each have a better chance of winning. If there’s time, bookmakers will adjust the prices available so that any new bets placed reflect this increased chance. However, if you place your bet before the horse withdraws and your bet goes on to win, we need to adjust your returns. This is industry-wide practice, and is known as a ‘Rule 4’ deduction.

-

Rule 4 deductions only occur when a horse is withdrawn from the race after the final declaration stage and before coming under starter’s orders. Final declarations are usually 24hrs before the race, but can sometimes be 48hrs before.

-

Usually a Rule 4 only applies if you took a price on your horse, but sometimes SP bets (what is an SP bet?) can be affected if the withdrawal was very, very last-minute.

-

In multiple bets, the deduction only applies to the parts of the bet specifically involving the withdrawn horse.

How will I know if a Rule 4 has been applied to my bet?

You'll see a bet message in My Bets, under an affected selection (see below image). The message will tell you the deduction amount (X pence in the £ - what does that mean?), and provide you with a link to this Help article.

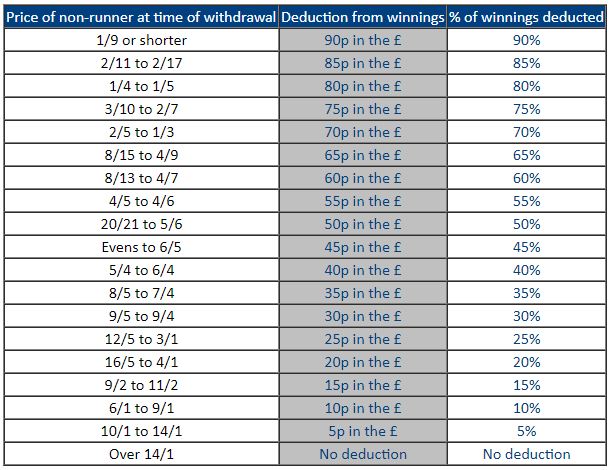

How is the Rule 4 amount calculated?

The exact amount deducted relates to the price of the non-runner, and is usually shown as a deduction of x pence in the pound.

This states the amount of money that’s taken from each £1 in winnings - so if you expected to win £10 but there’s a 10p Rule 4 deduction, your winnings will actually be £9.

The deduction amount depends on how likely the non-runner was to win - if a favourite withdraws, the deduction is bigger than if an outsider withdraws. This is because without the favourite in the race, the other horses have a much better chance of winning than they did before. Whereas if an outsider withdraws, it has less effect on the other horses’ chances. For withdrawn horses with prices bigger than 14/1, they were already very unlikely to win the race - so no deduction is made.

This table shows the industry-standard deductions that apply depending on the price of the non-runner:

Do you have a sample calculation?

Yes - here’s an example:

- You’ve placed a £20 bet on Horse A @ 7/4 in the 16.00 at Kempton, which has 6 runners.

- Your expected returns are £55 (winnings of £35 + your £20 stake)

- Later in the day, Horse B @ 4/1 withdraws from the race.

- It’s now a 5-runner race, and immediately your horse's chance of winning has increased from 1 in 6 runners to 1 in 5 runners.

- Once the non-runner is official, we revise the race as soon as possible with new odds for the 5 remaining runners: the revised price for Horse A is 5/4.

- But you already placed your bet at 7/4: this is no longer a fair reflection of Horse A's chances so if your horse wins, a Rule 4 will be applied to compensate. The Rule 4 deduction will be 20p in the £ (as the withdrawn horse was 4/1).

Your horse wins! Congratulations! Here’s how we calculate your adjusted returns:

- Your expected winnings were £35.

- Deduct 20p in the £ (i.e. 20%) of £35.00 = deduction of £7.

- Your adjusted winnings are £35 - £7 = £28

- £28 adjusted winnings + £20.00 stake = £48.00

- Your winning £20 bet @ 7/4 with a rule 4 of 20p will return you £48.00.

What happens if there’s more than one non-runner?

More than one Rule 4 deduction can apply if more than one horse withdraws from a race, but the total deductions won't exceed 90p in the £.

Rule 4 doesn’t apply to ante-post bets (bets placed before the final declaration stage), which is one of the main benefits of betting ante-post.

The main drawback, though, is that if your horse is a non-runner and you’ve bet ante-post, then you won’t get your stake back.

Click here to read more about ante-post betting.

‘Rule 4’ originates from Tattersall’s Rules of Betting (a list of rules devised in 1886 to govern racing), which are a longstanding part of horse racing betting in the UK and Ireland.

It’s called ‘Rule 4’ as it’s number 4 on the list.

1. If a horse is withdrawn and a new market is formed, all bets placed at show prices prior to the new market will be subject to the above deductions.

2. If two or more horses are withdrawn before coming under starter's orders, the total deductions shall not exceed 90p in the £.

3. If further horses are withdrawn after a new market has been formed, bets placed at show prices prior to a new market being formed will be subject to a further deduction based on the prices of all withdrawn horses.

4. Bets placed in the new market will be subject to a deduction based on the current price.

5. If the total deduction on the market is 5p in the £, the deduction will be waived.

6. Rule 4 deductions apply both to win bets and each way/place bets. But only your winnings are affected by the Rule 4 deduction, not your original stake.